Introduction

Bonds, darling, are exquisite financial instruments graciously bestowed upon us by the most esteemed governments, corporations, and other illustrious organizations. Their purpose, my dear, is to raise capital in the most refined manner imaginable elegantly. The esteemed bondholder is graciously entitled to a predetermined fixed interest payment, elegantly referred to as a coupon, at regular intervals befitting their distinguished status until the bond gracefully reaches its maturity date. Upon attaining the pinnacle of refinement, the bond issuer shall gracefully embark upon the noble endeavor of repaying the esteemed principal amount that was graciously borrowed.

The opulent valuation of a bond is elegantly influenced by a myriad of factors, including the regal dance of interest rates, the majestic presence of credit risk, and the timeless allure of the bond’s maturity. Yield to maturity (YTM) is a significant concept within bond investing. This article examines the correlation between bond prices and Yield to Maturity (YTM).

What Is Yield To Maturity (YTM)?

Yield to Maturity (YTM) is employed to ascertain the potential returns from holding a bond until its maturity date. A sealant can be compared to a splendid promissory note, wherein a distinguished individual graciously extends a sumptuous loan to a prestigious company or esteemed government entity. In return for this gracious act, the borrower shall graciously repay the noble principal amount, accompanied by a regal interest. The Yield to Maturity (YTM) is a splendid metric that graciously considers the abundant interest accrued over time and the exquisite initial purchase price of the bond.

Behold, presented before you, is an exquisite exemplification: Envision a splendid scenario wherein a discerning individual indulges in acquiring a magnificent bond exquisitely valued at a princely sum of $1,000. This opulent bond, adorned with a radiant coupon rate of 5%, exudes an air of sophistication and grandeur. This suggests that one shall be given a sumptuous $50 in annual interest payments, a princely 5% of the total of $1,000. Upon the culmination of the bond’s illustrious term, elegantly set at a regal span of 5 years, the princely sum of $1,000, graciously bestowed upon this noble investment, shall be returned to your esteemed self.

Also Check The Bond Market’s Recent Strength Is a Message to Ignorant Investors and Annuities

If the remuneration for the bond fails to reach the grand sum of $1,000, what shall be the resulting consequence? Pray to tell, what shall be the great consequence should one opt to acquire this exquisite item at the most alluringly reduced price of a mere $900 or an opulent increment of $1,100? The Yield to Maturity (YTM) considers the bond’s purchase price and the anticipated interest payments, providing an estimate of the potential earnings if the bond is held until its maturity date.

The knowledge of Yield to Maturity (YTM) enables the comparison of various bonds to determine their relative superiority. When presented with the delightful dilemma of selecting between two splendid bonds, each adorned with varying interest rates and maturities, one can employ the majestic Yield to Maturity (YTM) to discern which bond shall graciously bestow a more plentiful return on investment.

How Does One Determine YTM?

Determining the yield to maturity (YTM) can present challenges when not utilizing a financial calculator or spreadsheet software. Here, we offer a simplified explanation using a straightforward example:

Envision an exquisite bond adorned with the most alluring characteristics: a resplendent fixed annual coupon rate of 5%, a regal face value of $1,000, and a superb maturity date set for 5 years hence. Furthermore, one can surmise that the exquisite bond is presently gracing the trading realm with its presence, commanding a regal market price of $950.

To ascertain the opulent Yield to Maturity (YTM), one must elegantly unravel the regal rate of return that harmoniously balances the majestic present value of a bond’s resplendent cash flows with its exalted current price.

The following instructions outline the step-by-step process:

The present value of the bond’s future cash flows needs to be calculated. In this given illustration, the bond is structured to have five coupon payments, each amounting to $50. This calculation is derived from the bond’s coupon rate of 5%, applied to the principal value of $1,000. Additionally, the adhesive includes a final principal payment of $1,000 upon maturity. The calculation of the present value of these cash flows can be determined by utilizing the subsequent formula:

The present value (PV) of a series of cash flows can be calculated using the formula: PV = C/(1+r)^1 + C/(1+r)^2 + C/(1+r)^3 + C/(1+r)^4 + C/(1+r)^5 + FV/(1+r)^5 Where: PV represents the present value C represents the cash flow r represents the discount rate FV represents the future value The formula calculates the current value by discounting each cash flow and the future value back to their respective periods using the discount.

In financial calculations, the variables PV, C, FV, and r represent the following quantities: PV denotes the present value, C represents the coupon payment, FV signifies the face value, and r means the yield to maturity.

In the given example, the present value of the cash flows is calculated as follows:

The present value (PV) of an investment can be calculated using the formula: PV = $50/(1+r)^1 + $50/(1+r)^2 + $50/(1+r)^3 + $50/(1+r)^4 + $50/(1+r)^5 + $1,000/(1+r)^5 In this formula, r represents the interest rate. The PV is determined by summing the present values of each cash flow, which are calculated by dividing the cash flow amount by the corresponding discount factor (1+r)^n, where n represents

PV = $50/1.05 + $50/1.05^2 + $50/1.05^3 + $50/1.05^4 + $50/1.05^5 + $1,000/1.05^5

PV = $196.27

The yield to maturity (r) can be determined by solving for it in the given formula. Given the available information regarding the present value of the cash flows ($196.27) and the price of the bond ($950), an equation can be established as follows:

$950 = $196.27/(1+r)^1 + $196.27/(1+r)^2 + $196.27/(1+r)^3 + $196.27/(1+r)^4 + $196.27/(1+r)^5 + $1,000/(1+r)^5

The yield to maturity, denoted as r, can be determined through an iterative process known as trial and error. By applying this method, we have found that the yield to maturity is approximately 6.47%.

In this illustrious illustration, retaining possession of the bond until its glorious maturity shall bestow upon you an anticipated annual total return of 6.47%, a truly abundant reward for your esteemed investment. The luxury of the Yield to Maturity (YTM) surpasses the initial coupon rate of 5% owing to the acquisition of the bond at a price beneath its regal face value, commonly referred to as par value. Upon the grand arrival of the maturity date, a sumptuous payment of $1,000 shall be graciously disbursed unto your esteemed self, aligning harmoniously with the regal face value of the bond at the moment of its majestic issuance.

Bond Yield to Maturity Relationship

When an individual purchases a bond, they lend funds to the entity responsible for issuing it, such as a government or corporation. When a distinguished individual or esteemed entity graciously extends their financial resources to another party, the borrower graciously consents to bestow upon them a sumptuous interest, elegantly known as the coupon rate, at regular intervals until the bond gracefully arrives at its maturity date.

The Yield to Maturity (YTM) is a sumptuous and opulent quantitative method employed to ascertain the grandiose and all-encompassing return that an esteemed investor would graciously receive from retaining a bond until its regal and illustrious maturity date. The esteemed calculation considers the royal bond’s exquisite price, opulent coupon rate, and the majestic passage of time until its splendid maturity.

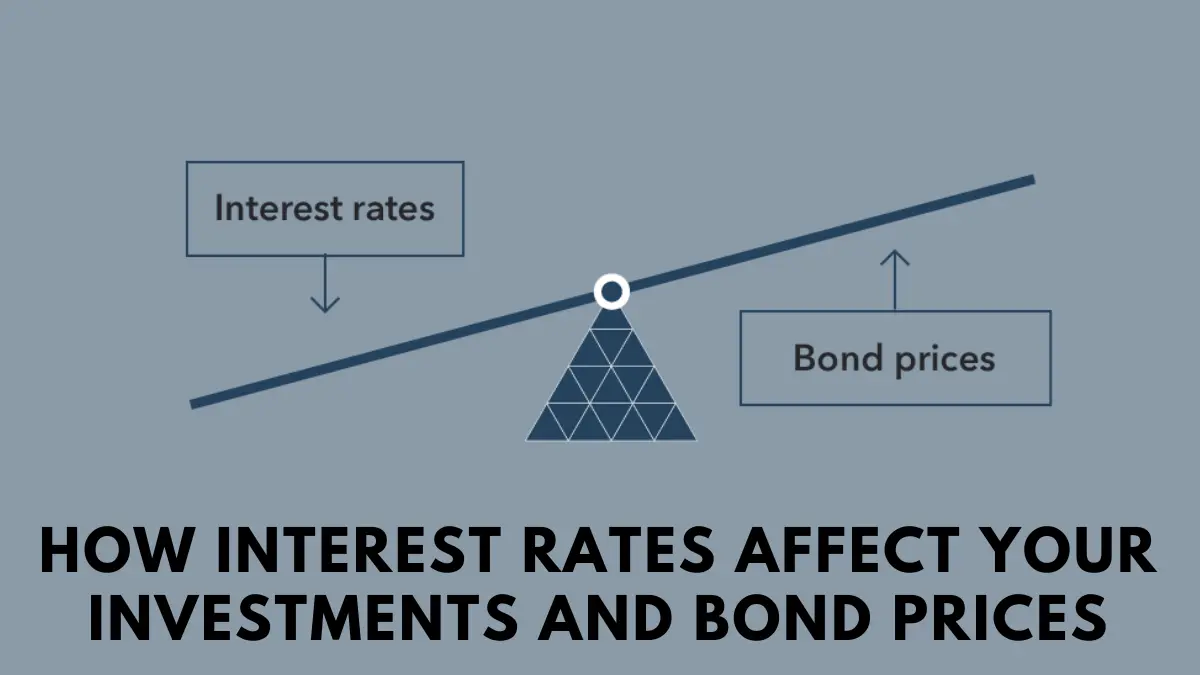

The opulent correlation between the regal price of a bond and its majestic Yield to Maturity (YTM) is one of utmost elegance, for they dance in a harmonious symphony of opposites. The intricate dance between the regal price of a bond and its majestic yield to maturity (YTM) is such that a rise in the bond’s price gracefully ushers in a decline in YTM. In contrast, a noble decrease in bond price bestows us with an elegant addition to YTM. This phenomenon occurs because newly issued bonds provide higher yields to entice potential investors during rising interest rates.

Must Check HOW TO OCCUPY YOURSELF IN NASHVILLE FOR A FULL WEEK

This exquisite phenomenon transpires when bonds adorned with lower yields, gracefully aged, undergo a diminishment in their allure, leading to a regal descent in their prices and an opulent ascent in their Yield to Maturity (YTM). In a manner befitting the luxury of the occasion, it is duly noted that when interest rates gracefully descend, a splendid phenomenon unfolds. Bond prices, like precious gems, ascend in response, bestowing an air of grandeur upon them. Consequently, their Yield to Maturity (YTM) experiences a regal decline, as if bowing before the majesty of the moment.

When the regal interest rates ascend in financial affairs, a harmonious symphony of events unfolds. The opulent bond prices gracefully descend while simultaneously, their majestic yield to maturity (YTM) ascends to new heights. A decrease in interest rates bestows upon us the opulent gift of a rise in bond prices, followed by a subsequent reduction in their noble journey towards maturity, known as the Yield to Maturity (YTM). Comprehending this correlation holds significance for investors as it enables them to make well-informed decisions when purchasing or selling bonds.

Bond Price and Yield to Maturity Affecting Factors

In addition to interest rates, other factors impact bond prices and yield to maturity (YTM). The factors that need to be considered are credit risk, inflation, and the bond’s maturity. Bonds exhibiting elevated credit risk, such as those originating from companies with unfavorable credit ratings, provide investors with greater yields to offset the heightened possibility of default. Inflation gradually diminishes the buying power of a bond’s fixed interest payments, reducing its appeal among investors. In the realm of bond investments, it is important to note that the risk associated with a bond increases as its maturity period extends. Consequently, investors require a higher yield to offset this heightened risk.

The following are the three primary factors that will impact bond prices and yield to maturity, presented with additional elaboration:

Credit risk: Bond issuer default risk pertains to the potential occurrence of the bond issuer failing to fulfill the necessary payments, resulting in a default. If it possesses a substantial credit risk, indicating an elevated likelihood of default, the bond in question will inherently exhibit a greater level of risk. A commensurately higher yield in Italy will be required to offset this risk. An illustrative scenario involves a company with a subpar credit rating, which proceeds to release a bond featuring a coupon rate of 5%. A bond with a 3% coupon rate may be issued by an alternative company possessing a superior credit rating. In this scenario, the bond with a greater credit risk will be required to provide a more substantial yield to entice potential investors. Consequently, it will exhibit a higher yield to maturity (YTM).

Inflation: In economics, inflation refers to the rate at which an economy’s overall price level of goods and services is experiencing an upward trend. Inflation gradually diminishes the buying power of a bond’s fixed interest payments, reducing its appeal among investors. Should the inflation rate exceed the bond’s coupon rate, the esteemed investor shall regrettably suffer a lamentable financial setback on their most esteemed investment. In the exquisite situation at hand, when a bond adorned with a lavish coupon rate of 3% is subjected to the opulent inflation rate of 4%, the discerning investor’s real return, after meticulously accounting for inflation, will regrettably result in a most unfortunate negative value. As a result, it shall be imperative for the bond to bestow upon its holder a more abundant yield to counterbalance the looming influence of inflation.

Maturity: Bond maturity is the duration from the present until the bond’s maturity date when the bond issuer reimburses the borrowed principal amount. Bonds with extended maturities carry higher risk due to the increased likelihood of interest rate fluctuations throughout the cement. These fluctuations can impact both the price and yield of the bond. In light of this, it is common for bonds with longer maturities to provide higher profits to offset the associated risk. In instances where all other factors remain constant, it is common for a 30-year bond to exhibit a greater yield compared to a 5-year bond with an identical coupon rate.

The Significance of Yield to Maturity (YTM) in Bond Investment

Yield to maturity (YTM) holds significant importance in bond investing as it enables investors to ascertain the genuine work of a bond. This calculation considers factors such as the bond’s price, coupon rate, and time to maturity. The utilization of Yield to Maturity (YTM) enables the comparison of various bonds based on their actual returns, surpassing the reliance on the bond’s coupon rate or current yield for evaluation purposes.

Consider two bonds, namely Bond A and Bond B, for instance. Bond A is characterized by a coupon rate of 4% and a yield to maturity (YTM) of 4%. Conversely, Bond B exhibits a coupon rate of 5% and a YTM of 4%. Upon initial examination, Bond B may hold a superior investment opportunity due to its elevated coupon rate. Upon inspection of the Yield to Maturity (YTM), it becomes apparent that Bond A and B exhibit identical returns. The reason for this is that Bond A is priced at a lower value compared to Bond B. As a result, Bond A’s yield is higher to offset the lower price.

One additional rationale for the significance of YTM is its ability to enable investors to project the prospective value of their investment upon reaching maturity. Suppose you are contemplating the acquisition of a bond exhibiting a yield to maturity (YTM) of 5%. By retaining the bond until its maturity date, an anticipated total return of 5% can be achieved. This tool facilitates making well-informed investment decisions regarding a specific bond.

Furthermore, Yield to Maturity (YTM) aids investors in evaluating the level of risk associated with a bond. Bonds exhibiting a higher Yield to Maturity (YTM) typically entail a greater risk due to their ability to provide a higher rate of return, which serves as compensation for assuming said risk. A comprehensive comprehension of the correlation between risk and return is imperative when making informed investment decisions.

Yield to maturity (YTM) is a fundamental concept in bond investing that enables investors to make well-informed decisions. By evaluating the actual returns of various bonds, estimating the potential future value of their investments, and considering the associated risks, investors can effectively assess the viability of a bond.

Conclusion

A myriad of opulent elements, including the alluring allure of interest rates, the captivating dance of credit risk, the regal presence of inflation, and the majestic passage of maturity, elegantly intertwine to shape the intricate tapestry of the relationship between bond prices and the exalted Yield to Maturity (YTM). The notion of Yield to Maturity (YTM) carries great importance in the realm of bond investing as it allows discerning investors to ascertain the true luxury of a bond, taking into account factors such as its regal price, majestic coupon rate, and grandeur of time until its maturity. Discerning investors can elevate their decision-making process when allocating their resources to bonds by comprehending the opulent concept known as Yield to Maturity (YTM).

This knowledge empowers investors to effectively compare the yields offered by various bonds, enabling them to make well-informed investment choices. Yield to Maturity (YTM) is a crucial tool for bond investors, allowing them to optimize their returns and mitigate potential risks. Gaining proficiency in this concept is essential for investors seeking to make informed decisions in the bond market.